One of the most controversial elements of the recent health reform legislation embodied in the Patient Protection and Affordable Care Act (ACA) has been the individual mandate. The mandate works as a conditional tax: by 2016, when the tax is fully phased in, individuals who do not purchase insurance coverage will pay about $60 per month. Exemptions are provided for those for whom the cheapest insurance plan would be unaffordable.

Not only is the mandate the least popular component of health reform, it is the most legally vulnerable. This week the Supreme Court

Photo: Jason Speros

The Supreme Court will soon rule on the fate of Affordable Care Act's individual mandate that would require all citizens to purchase health care insurance.

heard arguments on the constitutionality of the mandate. The Justices must decide whether the Constitution's explicit provision of the power to regulate interstate commerce to the Federal government includes the power to regulate "inactivity" -- the failure to purchase health insurance, in this case.

In the event that they rule that the mandate is unconstitutional, they must then rule whether or not it is "severable" from the rest of the ACA. If the mandate is both ruled as unconstitutional and non-severable, the majority of the law will be dismantled.

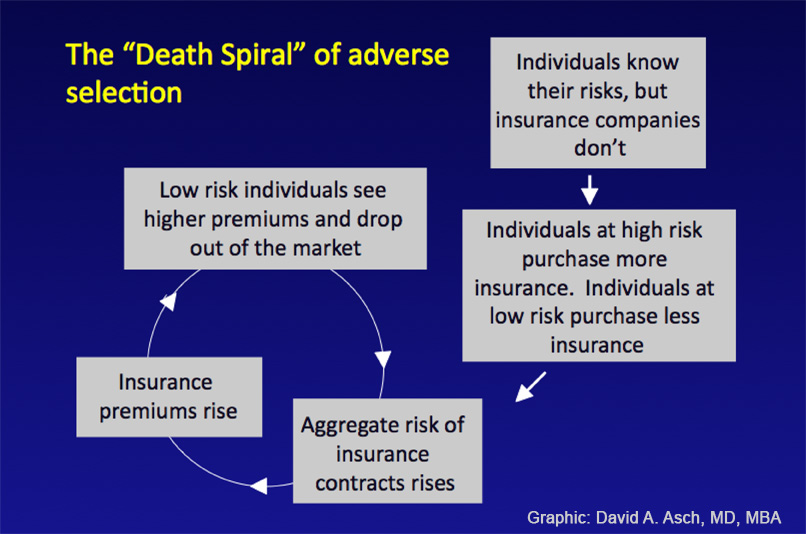

But what makes the mandate severable or not? The mandate would be severable if ACA sans-mandate wouldn't leave the insurance market with even more problems than it has today. To see if this will happen, we need to take a look at the economic theory that justified the mandate in the first place: adverse selection. We also need to see whether the theory holds up in reality.

The Economic theory Adverse selection is when sicker people are more likely to buy insurance than healthy people, and insurance companies are not able to adjust their premiums to account for the higher risk. This drives the average healthcare costs of the insurance plan higher, since the typical enrollee is sicker. This happens because people who buy insurance have more information about their likely health costs than insurance companies.

Adverse selection can also happen if insurers are prohibited from acting on information about patients -- like their gender or health status -- by raising their prices for sicker patients. These prohibitions are called "community rating" and "guaranteed issue," and are put in place to try to prevent insurers from making insurance too expensive for the chronically ill. The ACA implements community rating and guaranteed issue nationwide, which is one reason why the mandate was included in the bill.

One implication of adverse selection is that even if everyone wants insurance and is willing to pay more than their expected cost of medical care to obtain it, the market will not ensure that everyone is able to purchase insurance. Consequently,

Slide Presentation: Click to view "The Economics Behind The Individual Mandate" (5 minutes)

government intervention in the form of a subsidy or a mandate could improve the well-being of society as a whole.

'Death spiral' The worst-case scenario of adverse selection is a "death spiral." In a death spiral, prices rise so much that over time the person who last year decided that it was barely worth purchasing an insurance contract decides this year to forgo insurance and risk the financial burden of getting sick instead. If this happens year after year, only the very sickest are left insured -- and at very high prices.

Were that the entire story then very little data would be required to determine how important the mandate is to the overall health reform package. However, adverse selection does not have to exist in markets. Even when it does exist, adverse selection can be small enough that markets do not fall apart. Therefore, we have to examine the data to see what would happen if the Supreme Court strikes down the mandate.

The Massachusetts mandate The best test of the impact of an individual mandate is from the state of Massachusetts, which implemented statewide universal health care coverage in 2006. Its health reform plan was very similar to the Affordable Care Act: it included an individual mandate, subsidies to help lower income individuals afford insurance, and a health insurance exchange where individuals could easily search for and choose affordable insurance plans. The subsidies began in June 2007, and the mandate began to be enforced in December 2007.

Reform was very successful in reducing uninsurance rates in Massachusetts. Before the reform legislation, uninsurance rates were 20% among people with income below 300% of the federal poverty level (FPL). With the creation of the subsidies uninsurance fell to 14%, and after the mandate was implemented it was reduced to 2.6% among the total population, and to about 5% for people below 300% FPL.

Several studies have examined whether adverse selection was present in Massachusetts by looking at the impact of the individual mandate. Chandra, Gruber and McKnight (2011) considered enrollees in the Massachusetts private health insurance plan

Click for Larger Image

Figure 1 Shows the enrollment rates of both healthy and chronically ill Massachusetts consumers over time.

Commonwealth Care, and compared rates of chronic illness in enrollees in the periods both before and after the mandate went into effect. Figure 1 at left is the key figure from this study.

Figure 1 plots the enrollment rates of both healthy and chronically ill consumers over time. The second dotted line is December 2007, the month that the penalty for the mandate began to be assessed. As this figure shows, the rates of healthy enrollees increased more than the rate of chronically ill enrollment following the implementation of the mandate. Specifically, enrollees who signed up for insurance before the mandate went into effect were 50% more likely to be chronically ill and had 45% higher health care costs than individuals who signed up after the mandate was implemented. That means the mandate increased enrollment rates of enrollees who were healthier, thus reducing adverse selection.

This suggests that adverse selection was present in Massachusetts before the mandate, but what was the magnitude of its impact upon prices? Several studies have tried to estimate the effect of the mandate upon prices. They found that the individual mandate likely only led to a 3% decrease in the average price of premiums statewide.

However, this change is averaged across both the employer-based and individual insurance markets. Since most people don't choose their job based primarily on its insurance, adverse selection is much more significant in the individual market. Since the individual market is about 15% of the entire market for health insurance, an 18% decrease in prices in the individual market would cause the 3% overall change. Other evidence from Massachusetts suggests that prices in the individual markets fell by up to 20%. This is a large effect on prices and could be large enough to cause a death spiral in the individual health insurance market.

The bottom line If the Supreme Court rules the individual mandate unconstitutional, available evidence from Massachusetts suggests that eliminating it

but leaving the rest of the ACA intact would likely not cause a "death spiral" in premium prices nationwide. However, eliminating the mandate could potentially cause prices to rise significantly in the individual insurance markets, maybe even high enough to cause the market to unravel.

If the Supreme Court decides that this "death spiral" scenario is likely, they could rule that the mandate is not severable from the rest of the Affordable Care Act, and strike down the entire bill. Alternatively, they could eliminate the individual mandate along with a few other key provisions that cause adverse selection, like community rating and guaranteed issue.

We have only discussed the impact of the individual mandate on prices, and haven't talked about other benefits to society of lowering rates of uninsurance. If the Supreme Court strikes down the mandate, these potential benefits will be lost as well.

For instance, since hospitals are forced to stabilize any acutely ill person who needs treatment, striking down the mandate would lead to a continuation of the current situation, in which hospitals are forced to bear the costs of that uncompensated care. This is why states mandate car insurance -- to protect the party who was not responsible for the incident from having to pay for it if the person who caused the accident is not insured. Also, as we discussed earlier, even absent a death spiral, adverse selection means that people who want to buy health insurance -- and are willing to pay their fair share for it -- cannot.

Thus the individual mandate is based upon sound economic principles. However, economics are only one factor in the Supreme Court's decision. The justices must also consider issues of constitutionality, legal precedent, and the reach of congressional authority. If these legal issues cause them to rule against the mandate, a key policy tool initially proposed by Republicans to enable a market-based solution to the unique challenges of health insurance will be lost.

~ ~ ~

Ari Friedman is a University of Pennsylvania health economics MD/PhD student interested in health insurance and emergency medicine. Nora Becker is a third-year University of Pennsylvania health economics MD/PhD student interested in researching the impact of changes in health policy on costs and quality of care.

{kind=link}